1MDB Scandal: Have Malaysians Been Misled?

For more than a decade, Malaysians have been told that 1MDB was one of the country’s greatest financial scandals.

The narrative was simple and repeated relentlessly. Billions were allegedly lost, taxpayers were burdened, and the nation paid a heavy price.

That narrative may well contain substantial truth.

But a small disclosure buried within the Ministry of Finance’s First Quarter 2026 fiscal report raises a question that surprisingly remains unanswered after years of investigations, court proceedings, asset recoveries and political debate.

Have Malaysians ever been shown the complete financial picture?

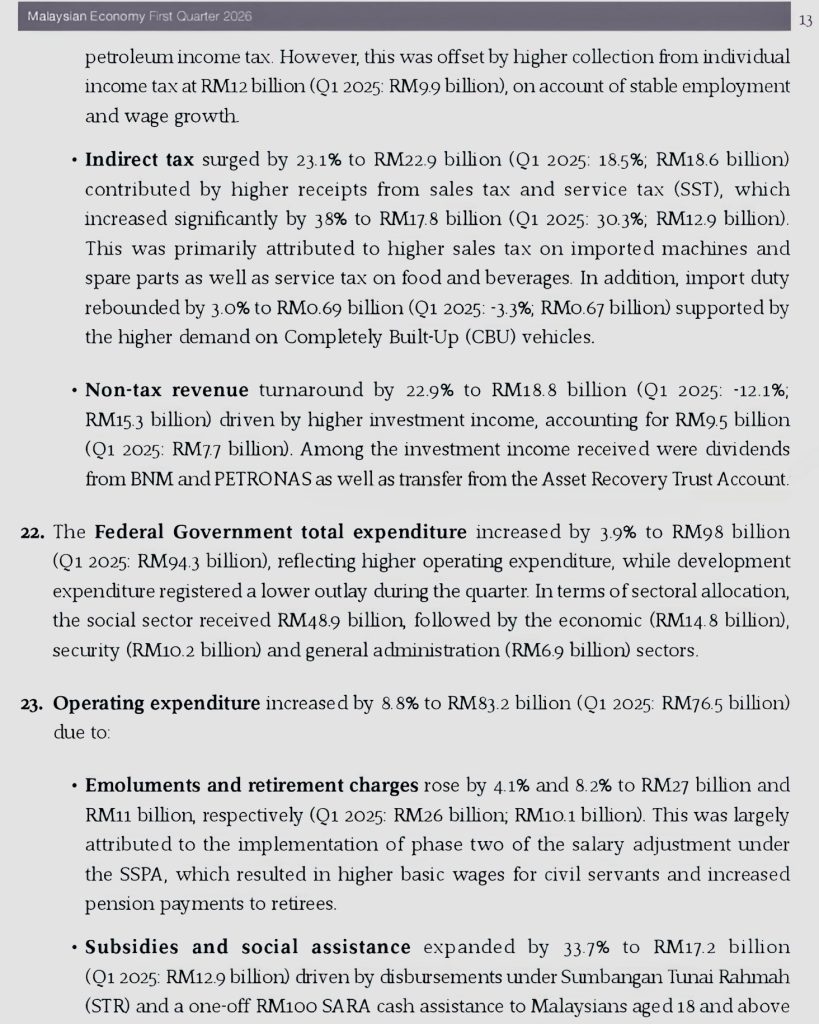

According to the report, Malaysia’s non-tax revenue increased by 22.9% to RM18.8 billion, supported by dividends from Bank Negara Malaysia, dividends from PETRONAS and a transfer from the Asset Recovery Trust Account.

At first glance, this appears to be a routine accounting disclosure.

In reality, it may be one of the most important developments relating to 1MDB in recent years.

The Question Raised by the Asset Recovery Trust Account

The significance lies in the nature of the account itself.

The Asset Recovery Trust Account was established in December 2018 specifically to receive and manage funds recovered from 1MDB and SRC International-related cases. Over the years, billions of ringgit recovered through settlements, asset seizures, repatriations and legal actions have been deposited into the account.

For years, Malaysians were told that these recovered funds existed primarily to service obligations linked to 1MDB and SRC International.

As recently as late 2025, the Ministry of Finance stated in Parliament that funds held within the Asset Recovery Trust Account had not been utilised for operating expenditure or new development expenditure. The ministry explained that the account was tightly regulated and that recovered funds were being used solely to meet existing 1MDB and SRC commitments and debt obligations.

That position appeared straightforward.

Which is precisely why the latest fiscal report raises an obvious question.

If the Asset Recovery Trust Account exists primarily to meet 1MDB and SRC liabilities, why is a transfer from that account now appearing as a contributor to government revenue?

The government may well have a reasonable explanation.

But the public deserves to hear it.

What Changed?

The significance of the latest disclosure is not that recoveries exist.

Malaysians have known for years that billions of ringgit were recovered through various legal settlements and asset recovery efforts.

The more important question is what has changed since those earlier explanations were provided.

Has the government’s assessment of outstanding liabilities improved?

Have major obligations already been settled?

Has the account accumulated funds beyond what is required to meet remaining commitments?

Has there been a change in accounting treatment?

Or has the financial position of 1MDB evolved substantially from the picture that Malaysians have been presented over the past several years?

These questions matter because they go directly to the heart of an issue that has rarely been discussed comprehensively.

What is the true financial position of 1MDB today?

For years, public debate has focused overwhelmingly on liabilities.

Far less attention has been paid to recoveries, remaining assets, realised value and the broader financial position after more than a decade of legal actions, asset sales and debt repayments.

The Other Side of the Ledger

According to official disclosures, Malaysia has recovered approximately RM31.3 billion through various 1MDB and SRC-related asset recovery efforts.

These recoveries include funds repatriated from foreign jurisdictions, proceeds from asset seizures, settlements with financial institutions and numerous legal agreements reached over the years.

RM31.3 billion is not a trivial amount.

It represents one of the largest asset recovery exercises ever undertaken by the Malaysian government.

Yet recoveries are only one component of the equation.

There is also Bandar Malaysia.

The sale of Bandar Malaysia to PETRONAS through KLCC Holdings was reported to be worth approximately RM12 billion. Regardless of political perspective, this represents tangible value generated from an asset originally associated with 1MDB.

Then there is Tun Razak Exchange (TRX).

Ironically, one of the most criticised projects linked to 1MDB has evolved into one of Kuala Lumpur’s most prominent financial districts.

In June 2018, the Ministry of Finance itself stated that TRX could realise at least RM7.6 billion in value and contribute towards meeting financial obligations associated with the development.

Today, TRX is no longer a future proposal.

It is a functioning financial district that houses multinational corporations, generates economic activity, supports employment and contributes to Malaysia’s attractiveness as an investment destination.

When assessing the overall financial consequences of 1MDB, can the value created by TRX simply be ignored?

That is a legitimate question.

Recoveries Are Not the Same as Cash

To be clear, recoveries, realised asset sales and asset valuations are not necessarily identical.

A recovery deposited into the Asset Recovery Trust Account is not automatically equivalent to unrestricted government revenue.

Likewise, asset valuations may represent estimated value rather than immediately available cash.

The economic benefits generated by developments such as TRX are also distinct from direct financial recoveries.

These distinctions matter.

But acknowledging them does not weaken the case for transparency.

It strengthens it.

Because if recoveries, asset values, liabilities and economic benefits are all different, then Malaysians need a comprehensive accounting that explains how those figures interact and what the final outcome actually looks like.

Without that accounting, public debate risks becoming a contest of isolated numbers rather than an assessment of the complete financial picture.

Where Is the Complete Balance Sheet?

For years, Malaysians were repeatedly reminded that 1MDB carried debts of approximately RM32 billion following the change of government in 2018.

That figure became deeply embedded in public consciousness and was frequently cited as evidence of the scale of the problem.

Yet today, official disclosures show approximately RM31.3 billion has been recovered.

Substantial value has also been generated through transactions involving former 1MDB assets and through developments that continue to operate and generate economic activity.

The question, therefore, is not whether 1MDB generated a profit.

The question is whether Malaysians have ever been shown a complete accounting of the outcome.

Where is the consolidated balance sheet?

Where is the comprehensive reconciliation that combines total liabilities, total recoveries, realised asset sales, remaining assets, outstanding obligations and the current balance of the Asset Recovery Trust Account?

How much remains to be paid?

How much has already been recovered?

What assets remain?

What obligations remain outstanding?

What is the current net financial position after years of recoveries, asset sales, debt repayments and project completion?

Remarkably, despite years of investigations, court proceedings, parliamentary debates, asset recoveries and political battles, Malaysians have never been presented with a single comprehensive public accounting that brings all these figures together in one place.

Instead, the debate continues to revolve around fragments.

Debt figures appear in one discussion.

Recovery figures appear in another.

Asset values are discussed separately.

Economic benefits are often excluded entirely.

The result is a public conversation in which different sides frequently focus on different sections of what is ultimately the same balance sheet.

Time for Full Transparency

The latest fiscal report presents an opportunity to move beyond political narratives.

The question is no longer simply how much was allegedly lost.

The question is what remains after more than a decade of recoveries, asset sales, project completions and debt repayments.

If the Asset Recovery Trust Account was established to receive recovered 1MDB funds, and if transfers from that account are now contributing to government revenue, then Malaysians deserve a full explanation of the account’s balance, its remaining obligations and the rationale behind those transfers.

Transparency should not be controversial.

It should be expected.

For years, politicians asked Malaysians to focus on what was allegedly lost.

Today, after approximately RM31.3 billion has been recovered, after major transactions involving former 1MDB assets have generated substantial value, after TRX has matured into a major financial district and after transfers from the Asset Recovery Trust Account have appeared in government revenue figures, the public has a right to ask a different question.

Have Malaysians been misled about the full 1MDB story?

Until a complete balance sheet is presented to the public, that question will remain unanswered.